Angstrom L2 captures priority-fee MEV inside the Uniswap v4 hook and pays it out immediately. This note explains how the hook splits the tax between fee recipients and how liquidity providers receive their share. The first section summarizes the on-chain flow; the remainder reproduces the full compensation-price derivation used by the contracts.

How the Tax Flows to LPs

Snapshot state : beforeSwap stores the pre-swap tick and liquidity so the hook knows exactly which ranges were crossed.Compute base deltas : TickIteratorLib walks the crossed ticks to derive each range's token deltas.Solve for a uniform price : CompensationPriceFinder chooses a compensation price p* so makers are paid as if the entire swap cleared at that level, using the formulas derived below.Accrue rewards : PoolRewardsLib updates growth accumulators (rewardGrowthOutsideX128, globalGrowthX128) that mirror Uniswap v3/v4 fee accounting.Pay on exit : When LPs remove liquidity, afterRemoveLiquidity settles their accumulated native-token rewards. Integrators can also query getPendingPositionRewards mid-position.

The hook shares the tax between the pool creator, protocol treasury, and LPs according to the fee configuration stored in the factory. LP payouts always stay in the rollup's native asset, matching the currency that sequencers prioritize.

Detailed Compensation Price Derivation

This section ports the formal derivation from the contracts repository. It defines the compensation price p ⋆ p_\star p ⋆

Variables & Definitions

L i > 0 L_i > 0 L i > 0 i i i L i = x i y i L_i = \sqrt{x_i y_i} L i = x i y i x i , y i x_i, y_i x i , y i i i i p i > 0 p_{i} > 0 p i > 0 i i i p ⋆ > 0 p_\star > 0 p ⋆ > 0 B > 0 B > 0 B > 0 Given some liquidity L i L_i L i p p p x x x y y y x = L i ⋅ 1 p , y = L i ⋅ p x = L_i\cdot\frac{1}{\sqrt p}, y = L_i\cdot{\sqrt p} x = L i ⋅ p 1 , y = L i ⋅ p

To compute the net amount deltas required to cross a range i i i Δ x i = L i ( 1 p i − 1 p i + 1 ) , Δ y i = L i ( p i + 1 − p i ) \Delta x_i =L_i(\frac{1}{\sqrt{p_i}}-\frac{1}{\sqrt{p_{i+1}}}),\ \Delta y_i = L_i(\sqrt{p_{i+1}}-\sqrt{p_i}) Δ x i = L i ( p i 1 − p i + 1 1 ) , Δ y i = L i ( p i + 1 − p i )

X ^ , Y ^ > 0 \hat X, \hat Y > 0 X ^ , Y ^ > 0 p ⋆ ∉ [ a i , b i ] p_\star \notin [a_i, b_i] p ⋆ ∈ / [ a i , b i ] a i = max { p i , p start } , b i = min { p i + 1 , p end } a_i = \max\{p_i, p_{\text{start}}\}, b_i = \min\{p_{i+1}, p_{\text{end}}\} a i = max { p i , p start } , b i = min { p i + 1 , p end } a i ≤ b i a_i \le b_i a i ≤ b i

X ^ = ∑ i L i ( 1 a i − 1 b i ) , Y ^ = ∑ i L i ( b i − a i ) . \hat X =\sum_i L_i(\frac{1}{\sqrt{a_i}}-\frac{1}{\sqrt{b_i}}),\qquad \hat Y = \sum_i L_i(\sqrt{b_i}-\sqrt{a_i}). X ^ = ∑ i L i ( a i 1 − b i 1 ) , Y ^ = ∑ i L i ( b i − a i ) .

Compensation Price definition

Assuming unsigned total deltas X = ∑ i Δ x i , Y = ∑ i Δ y i X = \sum_i {\Delta x_i}, Y=\sum_i \Delta y_i X = ∑ i Δ x i , Y = ∑ i Δ y i p ⋆ p_\star p ⋆

Zero-for-One Swap: p ⋆ = Y X + B p_\star = \frac{Y}{X + B} p ⋆ = X + B Y i i i Δ x i ′ = Δ y i ⋅ ( min { p ⋆ , Δ y i Δ x i } ) − 1 \Delta x_i' = \Delta y_i \cdot (\min\{p_\star, \frac{\Delta y_i}{\Delta x_i}\})^{-1} Δ x i ′ = Δ y i ⋅ ( min { p ⋆ , Δ x i Δ y i } ) − 1

One-for-Zero Swap: p ⋆ = Y X − B p_\star = \frac{Y}{X- B} p ⋆ = X − B Y i i i Δ x i ′ = Δ y i ⋅ ( max { p ⋆ , Δ y i Δ x i } ) − 1 \Delta x_i' = \Delta y_i \cdot (\max\{p_\star, \frac{\Delta y_i}{\Delta x_i}\})^{-1} Δ x i ′ = Δ y i ⋅ ( max { p ⋆ , Δ x i Δ y i } ) − 1

Base Considered Swap Amount

Notice from the above definition that there will be a consecutive sub-set of ranges which will trade at (p ⋆ ≤ Δ y i Δ x i p_\star \le \frac{\Delta y_i}{\Delta x_i} p ⋆ ≤ Δ x i Δ y i p ⋆ ≥ Δ y i Δ x i p_\star \ge \frac{\Delta y_i}{\Delta x_i} p ⋆ ≥ Δ x i Δ y i

This range can be determined by walking from p s t a r t → p e n d p_{start} \rightarrow p_{end} p s t a r t → p e n d X ^ = ∑ i Δ x i , Y ^ = ∑ i Δ y i \hat X = \sum_i {\Delta x_i},\hat Y=\sum_i \Delta y_i X ^ = ∑ i Δ x i , Y ^ = ∑ i Δ y i p ~ i = Y ^ X ^ + B / p ~ i = Y ^ X ^ − B \tilde p_i = \frac{\hat Y}{\hat X + B}/\tilde p_i = \frac{\hat Y}{\hat X - B} p ~ i = X ^ + B Y ^ / p ~ i = X ^ − B Y ^ p ~ i \tilde p_i p ~ i

If all ranges are depleted and p ~ e n d \tilde p_{end} p ~ e n d p e n d p_{end} p e n d p ⋆ : = p ~ e n d p_\star := \tilde p_{end} p ⋆ := p ~ e n d

Otherwise when a range is found such that p ~ i ∈ [ p i , p i + 1 ] \tilde p_i \in [p_i, p_{i+1}] p ~ i ∈ [ p i , p i + 1 ] p ⋆ p_\star p ⋆

Zero-for-One (price decreasing)

Setup

For a given tick i i i

Δ x = L ( 1 p ⋆ − 1 p i + 1 ) , Δ y = L ⋅ ( p i + 1 − p ⋆ ) , B = Y ^ + Δ y p ⋆ − ( X ^ + Δ x ) . \Delta x = L\left(\frac{1}{\sqrt{p_\star}}-\frac{1}{\sqrt{p_{i+1}}}\right),\qquad

\Delta y = L\cdot(\sqrt{p_{i+1}}-\sqrt{p_\star}),\qquad

B = \frac{\hat Y+\Delta y}{p_\star} - (\hat X+\Delta x). Δ x = L ( p ⋆ 1 − p i + 1 1 ) , Δ y = L ⋅ ( p i + 1 − p ⋆ ) , B = p ⋆ Y ^ + Δ y − ( X ^ + Δ x ) . Quadratic in p ⋆ \sqrt{p_\star} p ⋆

Clearing denominators and simplifying yields:

A ⋅ ( p ∗ ⋆ ) 2 + 2 L ⋅ p ∗ ⋆ − ( Y ^ + y ) = 0 , A : = B + X ^ − x A \cdot(\sqrt{p*\star})^2 + 2L\cdot\sqrt{p*\star} - (\hat Y+y) = 0,\qquad A := B + \hat X - x A ⋅ ( p ∗ ⋆ ) 2 + 2 L ⋅ p ∗ ⋆ − ( Y ^ + y ) = 0 , A := B + X ^ − x

Solutions:

p ⋆ = − L ± L 2 + A ( Y ^ + y ) A = − L ± Y ^ ( B + X ^ − x ) + y ( B + X ^ ) B + X ^ − x . \begin{aligned}

\sqrt{p_\star} &= \frac{-L \pm \sqrt{L^2 + A(\hat Y + y)}}{A} \\

&= \frac{-L \pm \sqrt{\hat Y (B + \hat X - x) + y (B + \hat X)}}{B + \hat X - x}.

\end{aligned} p ⋆ = A − L ± L 2 + A ( Y ^ + y ) = B + X ^ − x − L ± Y ^ ( B + X ^ − x ) + y ( B + X ^ ) . (The two radicands are equal because L 2 = x y L^2=xy L 2 = x y

Existence & Uniqueness on ( 0 , u ] (0,u] ( 0 , u ] u = p i + 1 u=\sqrt{p_{i+1}} u = p i + 1

The quadratic gives us two solutions, we now want to prove the theorem that:

There exists one unique solution that lies in the range ( 0 , u ] (0, u] ( 0 , u ] s + = − L + L 2 + A ( Y ^ + y ) A s_+ = \frac{-L + \sqrt{L^2 + A(\hat Y+y)}}{A} s + = A − L + L 2 + A ( Y ^ + y )

Let's take the above quadratic as a function ϕ ( s ) \phi(s) ϕ ( s ) ϕ ( p ⋆ ) = 0 \phi(\sqrt{p_\star}) = 0 ϕ ( p ⋆ ) = 0

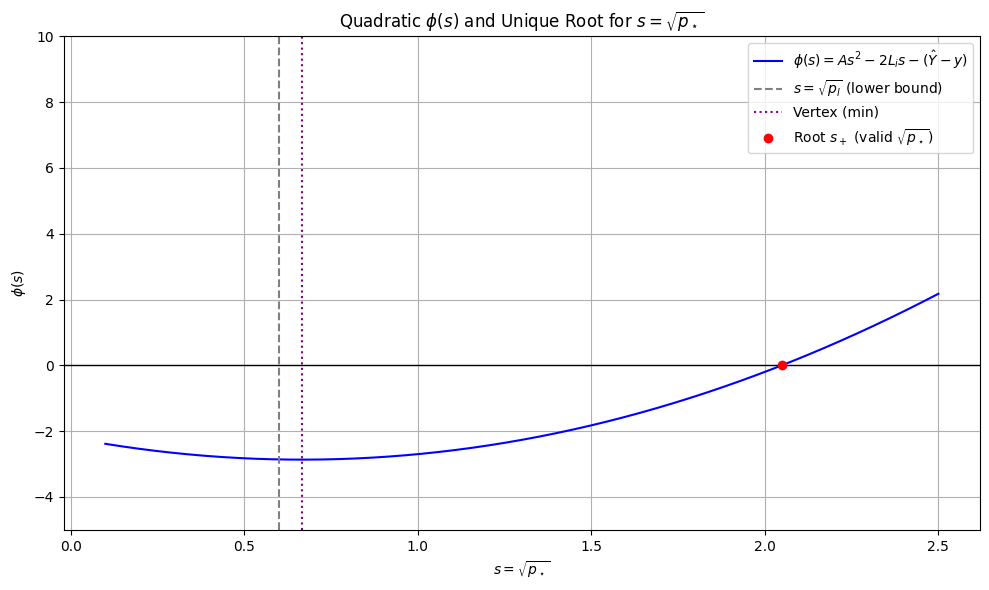

ϕ ( s ) = A s 2 + 2 L s − ( Y ^ + y ) \phi(s) =A s^2 + 2Ls - (\hat Y+y) ϕ ( s ) = A s 2 + 2 L s − ( Y ^ + y )

Lemma 1: Monotonicity of ϕ ( s ) \phi(s) ϕ ( s ) ( 0 , u ] (0,u] ( 0 , u ]

We prove that ϕ ( s ) \phi(s) ϕ ( s ) s ∈ ( 0 , u ] s \in (0, u] s ∈ ( 0 , u ] ϕ ′ ( s ) ≥ 0 \phi'(s) \ge 0 ϕ ′ ( s ) ≥ 0

ϕ ′ ( s ) = 2 A s + 2 L \phi'(s) = 2As + 2L ϕ ′ ( s ) = 2 A s + 2 L

ϕ ′ ( 0 ) ≥ 0 \phi'(0) \ge 0 ϕ ′ ( 0 ) ≥ 0 ϕ ′ ( 0 ) = 2 A ( 0 ) + 2 L = 2 L ⇒ ϕ ′ ( 0 ) ≥ 0 \phi'(0) = 2A(0) + 2L = 2L \Rightarrow \phi'(0) \ge 0 ϕ ′ ( 0 ) = 2 A ( 0 ) + 2 L = 2 L ⇒ ϕ ′ ( 0 ) ≥ 0

ϕ ′ ( u ) ≥ 0 \phi'(u) \ge 0 ϕ ′ ( u ) ≥ 0

Expand ϕ ′ ( u ) \phi'(u) ϕ ′ ( u ) 2 A u + 2 L ≥ 0 ⇔ 2 ( B + X ~ − x ) u ≥ − 2 L 2Au + 2L \ge 0 \Leftrightarrow 2 (B + \tilde X - x)u \ge -2L 2 A u + 2 L ≥ 0 ⇔ 2 ( B + X ~ − x ) u ≥ − 2 L

Prove tighter bound: B + X ~ − x ≥ − x ⇒ 2 ( − x ) u ≥ − 2 L ⇒ 2 A u ≥ − 2 L B + \tilde X - x \ge -x \Rightarrow 2(-x)u \ge -2L \Rightarrow 2Au \ge -2L B + X ~ − x ≥ − x ⇒ 2 ( − x ) u ≥ − 2 L ⇒ 2 A u ≥ − 2 L

Use u = y x u = \sqrt\frac{y}{x} u = x y 2 ( − x ) y x ≥ − 2 x y ⇔ x y x ≤ x y ⇔ x 2 y x = x y \quad 2 (-x)\sqrt{\frac{y}{x}}\ge -2\sqrt{xy}\Leftrightarrow x\sqrt{\frac{y}{x}}\le\sqrt{xy}\Leftrightarrow\sqrt{x^2\frac{y}{x}}=\sqrt{xy} 2 ( − x ) x y ≥ − 2 x y ⇔ x x y ≤ x y ⇔ x 2 x y = x y

Lemma 2: Boundary signs ϕ ( 0 ) < 0 \phi(0) < 0 ϕ ( 0 ) < 0 ϕ ( u ) ≥ 0 \phi(u) \ge 0 ϕ ( u ) ≥ 0

ϕ ( 0 ) < 0 \phi(0) \lt 0 ϕ ( 0 ) < 0 − ( Y ~ + y ) < 0 - (\tilde Y + y) < 0 − ( Y ~ + y ) < 0 ϕ ( u ) ≥ 0 \phi(u) \ge 0 ϕ ( u ) ≥ 0

Expand ϕ ( u ) \phi(u) ϕ ( u ) A u 2 + 2 L u − ( Y ~ + y ) ≥ 0 Au^2+2Lu-(\tilde Y + y) \ge 0 A u 2 + 2 Lu − ( Y ~ + y ) ≥ 0

Expand A A A ( B + X ^ − x ) u 2 + 2 y − Y ~ − y ≥ 0 ⇔ ( B + X ~ ) u 2 ≥ Y ~ (B + \hat X - x)u^2+2y-\tilde Y - y \ge 0 \Leftrightarrow (B + \tilde X)u^2 \ge \tilde Y ( B + X ^ − x ) u 2 + 2 y − Y ~ − y ≥ 0 ⇔ ( B + X ~ ) u 2 ≥ Y ~

Reorganize & expand u 2 u^2 u 2 p i + 1 ≥ Y ~ B + X ~ p_{i+1}\ge\frac{\tilde Y}{B + \tilde X} p i + 1 ≥ B + X ~ Y ~

Recognize that p ~ = Y ~ B + X ~ \tilde p = \frac{\tilde Y}{B + \tilde X} p ~ = B + X ~ Y ~ p i + 1 ≥ p ~ p_{i+1} \ge \tilde p p i + 1 ≥ p ~

Lemma 3: Unique Solution in ( 0 , u ] (0,u] ( 0 , u ]

Using Lemma 1 & 2 and the Intermediate value theorem we now know that there is exactly one s ∈ ( 0 , u ] s \in (0,u] s ∈ ( 0 , u ] ϕ ( s ) = 0 \phi(s) = 0 ϕ ( s ) = 0

Lemma 4: s + s_+ s +

s + = − L + D A , D : = L 2 + A ( Y ^ + y ) s_+ = \frac{-L + \sqrt{D}}{A}, D:=L^2 + A(\hat Y+y) s + = A − L + D , D := L 2 + A ( Y ^ + y ) s − = − L − D A s_- = \frac{-L - \sqrt{D}}{A} s − = A − L − D

A > 0 A > 0 A > 0 s − < 0 s_- < 0 s − < 0 s + s_+ s +

A < 0 A < 0 A < 0

When A < 0 A < 0 A < 0 D < L \sqrt D < L D < L s + s_+ s + s − s_- s −

s + < s − s_+ < s_- s + < s − − L + D A < − L − D A \frac{-L + \sqrt{D}}{A} < \frac{-L - \sqrt{D}}{A} A − L + D < A − L − D − L + D > − L − D -L + \sqrt{D} > -L - \sqrt{D} − L + D > − L − D D > − D \sqrt{D} > - \sqrt{D} D > − D

All together

Together we've shown that there is always a positive solution for p ⋆ \sqrt {p_\star} p ⋆ 0 0 0 p i + 1 \sqrt{p_{i+1}} p i + 1

One-for-Zero (price increasing)

For a given tick i i i

Δ x = L ( 1 p i − 1 p ⋆ ) , Δ y = L ⋅ ( p ⋆ − p i ) , B = ( X ^ + Δ x ) − Y ^ + Δ y p ⋆ . \Delta x = L\left(\frac{1}{\sqrt{p_i}}-\frac{1}{\sqrt{p_\star}}\right),\qquad\Delta y = L\cdot(\sqrt{p_\star}-\sqrt{p_i}),\qquad B = (\hat X+\Delta x) - \frac{\hat Y+\Delta y}{p_\star}. Δ x = L ( p i 1 − p ⋆ 1 ) , Δ y = L ⋅ ( p ⋆ − p i ) , B = ( X ^ + Δ x ) − p ⋆ Y ^ + Δ y .

Quadratic in p ⋆ \sqrt{p_\star} p ⋆

Clearing denominators, substituting A : = X ~ + x − B A := \tilde X + x - B A := X ~ + x − B s : = p ⋆ s := \sqrt{p_\star} s := p ⋆

A s 2 − 2 L s − ( Y ~ − y ) = 0 As^2 - 2Ls - (\tilde Y - y) = 0 A s 2 − 2 L s − ( Y ~ − y ) = 0

Solutions:

p ⋆ = L ± L 2 + A ( Y ^ − y ) A = L ± Y ^ ( x + X ^ − B ) − y ( X ^ − B ) x + X ^ − B . \begin{aligned}

\sqrt{p_\star} &= \frac{L \pm \sqrt{L^2 + A(\hat Y - y)}}{A} \\

&= \frac{L \pm \sqrt{\hat Y (x + \hat X - B) - y (\hat X - B)}}{x + \hat X - B}.

\end{aligned} p ⋆ = A L ± L 2 + A ( Y ^ − y ) = x + X ^ − B L ± Y ^ ( x + X ^ − B ) − y ( X ^ − B ) . Lemma 1: Monotonicity in range [ l , + ∞ ) [l, +\infty) [ l , + ∞ ) l = p i l = \sqrt{p_i} l = p i

ϕ ′ ( s ) = 2 A s − 2 L ϕ ′ ( s ) ≥ 0 ⇔ s ≥ L A \begin{aligned}

\phi'(s) &= 2As - 2L \\

\phi'(s) \ge 0 &\Leftrightarrow s \ge \frac{L}{A}

\end{aligned} ϕ ′ ( s ) ϕ ′ ( s ) ≥ 0 = 2 A s − 2 L ⇔ s ≥ A L We'll call the point L A \frac L A A L ϕ ( s ) \phi(s) ϕ ( s ) s 0 s_0 s 0 [ l , + ∞ ) [l, +\infty) [ l , + ∞ )

Lemma 2: Negative Lower Range Bound ϕ ( s 0 ) ≤ 0 \phi(s_0) \le 0 ϕ ( s 0 ) ≤ 0

ϕ ( s 0 ) ≤ 0 A ( L A ) 2 − 2 L ( L A ) − ( Y ~ − y ) ≤ 0 − L 2 A − ( Y ~ − y ) ≤ 0 − L 2 A ≤ Y ~ − y − L 2 ≤ ( Y ~ − y ) A − L 2 ≤ Y ~ A − y ( X ~ − B ) − y x 0 ≤ Y ~ A − y ( X ~ − B ) y ( X ~ − B ) ≤ Y ~ A \begin{aligned}

\phi(s_0) &\le 0 \\

A\left(\frac{L}{A}\right)^2 - 2L\left(\frac{L}{A}\right) - (\tilde Y - y) &\le 0 \\

-\frac{L^2}{A} - (\tilde Y - y) &\le 0 \\

-\frac{L^2}{A} &\le \tilde Y - y \\

-L^2 &\le (\tilde Y - y) A \\

-L^2 &\le \tilde Y A - y (\tilde X - B) - yx \\

0 &\le \tilde Y A - y (\tilde X - B) \\

y (\tilde X - B) &\le \tilde Y A

\end{aligned} ϕ ( s 0 ) A ( A L ) 2 − 2 L ( A L ) − ( Y ~ − y ) − A L 2 − ( Y ~ − y ) − A L 2 − L 2 − L 2 0 y ( X ~ − B ) ≤ 0 ≤ 0 ≤ 0 ≤ Y ~ − y ≤ ( Y ~ − y ) A ≤ Y ~ A − y ( X ~ − B ) − y x ≤ Y ~ A − y ( X ~ − B ) ≤ Y ~ A X ~ − B < 0 \tilde X - B < 0 X ~ − B < 0

Reorganize into fractions: y A ≥ Y ~ X ~ − B \frac y A \ge \frac {\tilde Y}{\tilde X - B} A y ≥ X ~ − B Y ~

Trivially true because y > 0 , A > 0 , Y ~ > 0 y > 0, A > 0, \tilde Y > 0 y > 0 , A > 0 , Y ~ > 0

X ~ − B > 0 \tilde X - B > 0 X ~ − B > 0

Reorganize into fractions: y x + ( X ~ − B ) ≤ Y ~ X ~ − B \frac y {x + (\tilde X - B)} \le \frac {\tilde Y}{\tilde X - B} x + ( X ~ − B ) y ≤ X ~ − B Y ~

Tighten inequality: y x ≤ Y ~ X ~ − B \frac y x \le \frac {\tilde Y}{\tilde X - B} x y ≤ X ~ − B Y ~

Trivially true as it's the pre-condition to the computation

Lemma 3: Unique solution in [ s 0 , + ∞ ) [s_0, +\infty) [ s 0 , + ∞ )

Using the above lemmas together with a intermediate value theorem we now know that there is a unique solution in this range.

Lemma 4: s + ∈ [ s 0 , + ∞ ) s_+ \in [s_0, +\infty) s + ∈ [ s 0 , + ∞ )

D : = L 2 + A ( Y ^ − y ) s + = L + D A s − = L − D A \begin{aligned}

D &:= L^2 + A(\hat Y - y) \\

s_+ &= \frac{L + \sqrt{D}}{A} \\

s_- &= \frac{L - \sqrt{D}}{A}

\end{aligned} D s + s − := L 2 + A ( Y ^ − y ) = A L + D = A L − D When Y ^ − y ≥ 0 \hat Y-y \ge 0 Y ^ − y ≥ 0

A ( Y ~ − y ) ≥ 0 ⇒ D ≥ L 2 ⇒ D ≥ L A(\tilde Y - y) \ge 0 \Rightarrow D \ge L^2 \Rightarrow \sqrt D \ge L A ( Y ~ − y ) ≥ 0 ⇒ D ≥ L 2 ⇒ D ≥ L Trivially: s − < 0 s_- < 0 s − < 0 s + s_+ s +

When Y ^ − y < 0 \hat Y-y \lt 0 Y ^ − y < 0

D < L \sqrt D \lt L D < L s + s_+ s + s − s_- s − However we can trivially see that s + > s − s_+ > s_- s + > s −

Because exactly one solution must lie in [ s 0 , + ∞ ) [s_0, +\infty) [ s 0 , + ∞ ) s + s_+ s + s − s_- s − s + > s − s_+ > s_- s + > s − s + ∉ [ s 0 , + ∞ ) s_+ \notin [s_0, +\infty) s + ∈ / [ s 0 , + ∞ )

Lemma 5: s + ≥ l s_+ \ge l s + ≥ l

L + D A ≥ l L + D ≥ l ( x + X ~ − B ) L + D ≥ L + l ( X ~ − B ) D ≥ l ( X ~ − B ) \begin{aligned}

\frac{L + \sqrt{D}}{A} &\ge l \\

L + \sqrt{D} &\ge l (x + \tilde X - B) \\

L + \sqrt{D} &\ge L + l (\tilde X - B) \\

\sqrt{D} &\ge l (\tilde X - B)

\end{aligned} A L + D L + D L + D D ≥ l ≥ l ( x + X ~ − B ) ≥ L + l ( X ~ − B ) ≥ l ( X ~ − B ) When X ~ − B < 0 \tilde X - B < 0 X ~ − B < 0

When X ~ − B ≥ 0 \tilde X -B \ge 0 X ~ − B ≥ 0

D ≥ p i ( X ~ − B ) 2 L 2 + A ( Y ~ − y ) ≥ p i ( X ~ − B ) 2 L 2 + A Y ~ − y x − y ( X ~ − B ) ≥ p i ( X ~ − B ) 2 A Y ~ − y ( X ~ − B ) ≥ p i ( X ~ − B ) 2 A Y ~ ≥ p i ( X ~ − B ) 2 + y ( X ~ − B ) A Y ~ ≥ p i ( X ~ − B ) 2 + p i x ( X ~ − B ) A Y ~ ≥ p i ( X ~ − B ) ( ( X ~ − B ) + x ) Y ~ X ~ − B ≥ p i p ~ ≥ p i \begin{aligned}

D &\ge p_i (\tilde X - B)^2 \\

L^2 + A (\tilde Y - y) &\ge p_i (\tilde X - B)^2 \\

L^2 + A \tilde Y - yx - y(\tilde X - B) &\ge p_i (\tilde X - B)^2 \\

A \tilde Y - y(\tilde X - B) &\ge p_i (\tilde X - B)^2 \\

A \tilde Y &\ge p_i (\tilde X - B)^2 + y(\tilde X - B) \\

A \tilde Y &\ge p_i (\tilde X - B)^2 + p_i x(\tilde X - B) \\

A \tilde Y &\ge p_i (\tilde X - B)\big((\tilde X - B) + x\big) \\

\frac{\tilde Y}{\tilde X - B} &\ge p_i \\

\tilde p &\ge p_i

\end{aligned} D L 2 + A ( Y ~ − y ) L 2 + A Y ~ − y x − y ( X ~ − B ) A Y ~ − y ( X ~ − B ) A Y ~ A Y ~ A Y ~ X ~ − B Y ~ p ~ ≥ p i ( X ~ − B ) 2 ≥ p i ( X ~ − B ) 2 ≥ p i ( X ~ − B ) 2 ≥ p i ( X ~ ��− B ) 2 ≥ p i ( X ~ − B ) 2 + y ( X ~ − B ) ≥ p i ( X ~ − B ) 2 + p i x ( X ~ − B ) ≥ p i ( X ~ − B ) ( ( X ~ − B ) + x ) ≥ p i ≥ p i This is the precondition for the calculation which makes our lemma s + ≥ l s_+ \ge l s + ≥ l

Final Proposition

Thanks to lemmas 3-5 we have now proven the required facts to know that s + s_+ s + p ⋆ \sqrt{p_\star} p ⋆